Division 296 tax significantly changes how defined benefit superannuation interests are valued and taxed. It matters mostly for higher‑income members and pensioners whose notional super balances approach or exceed the new $3 million (and $10 million) thresholds.

A central implication is that defined benefit interests will be re‑valued annually under prescribed methods, typically based on family‑law style actuarial factors, rather than the old static “pension × 16” approach or withdrawal values.

These new rules apply to both defined benefit pensions in payment and defined benefit interests still accruing, and are designed to give the ATO a more realistic, standardised total superannuation balance (TSB) figure for each member.

While the ATO has yet to finalise the methodology, indicative estimates are available using your member statement and our Family Law valuation page here – with the option to order a formal valuation.

Using risk optimisation techniques gained from over 25+ years experience in aggregating insurance risks, connectingthedots is able to "cherry pick" the ASX and apply the same techniques to investment portfolios.

This gives an average return for Australian equities of 30% per annum since 2017 with 17% in the last year. This is achieved by applying our Investment Strategy and by systematically optimising the risk-return balance across the portfolio over regular time periods. When managed actively, these returns can be boosted by an additional 10-20% p.a.

Our cumulative performance is set out in more detail in the chart following (passive strategy):

This performance compares more than favourably to that for all MySuper funds with an average of 7.2% for the last 10 years.

This methodology is reflected in our Corporate Investment Strategy.

Access to these returns is only available to our shareholders and employees via our superannuation fund. Existing clients may track our current portfolio by entering their client code in the righthand margin.

All our applications are built in R using shiny-server. Consultation services are available to wholesale and corporates via our contact form.

The Australian Prudential Regulatory Authority (APRA) surveys all MySuper funds each year for performance via annual statistical returns. This forms part of an annual superannuation performance test. Looking at the Fund Level data in the latest Annual Survey of MySuper funds - released in December 2025 - the average fund return was 7.2% p.a. for balanced funds over the last 10 years (after fees) to 30 June 2025.

The Australian Government has announced the commencement of the Family Law (Superannuation) Regulations 2025, marking a significant update to the legal framework governing the division of superannuation assets during family law proceedings. The new regulations, which came into effect from 1st April 2025, replace the Family Law (Superannuation) Regulations 2001 and are designed to ensure the continued fair and accurate treatment of superannuation in the context of relationship breakdowns.

Alongside the new regulations, the Family Law (Superannuation) (Methods and Factors for Valuing Particular Superannuation Interests) Approval 2025 has also commenced. This instrument, approved by the Attorney-General, details the specific actuarial methods and factors to be used in valuing superannuation interests for family law purposes. It maintains continuity with previous methods while allowing for technical updates and future reviews

connectingthedots is pleased to renew its actuarial certificate service with BGL SimpleFund360. Account balances and transactions are compiled in real time and presented as charts instantly. No data entry required and all without passwords.

All our certificates are reviewed by our actuary owner and users can review fund balances across the current tax year in real time as follows:

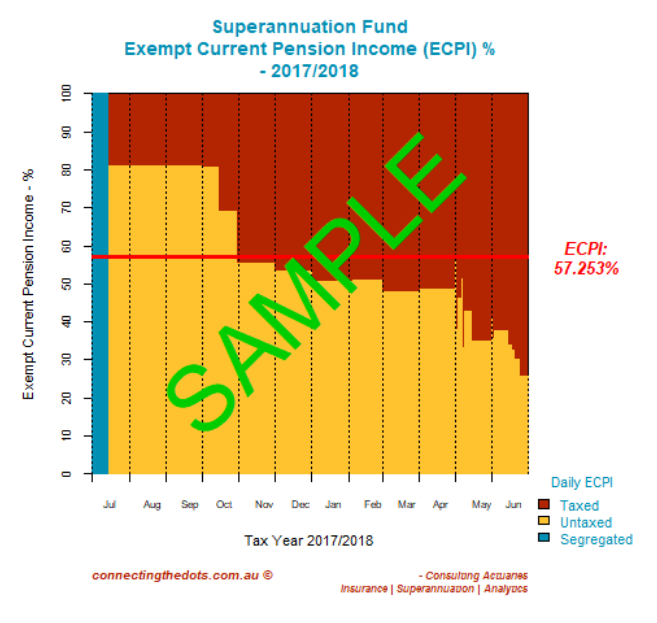

Then the results are presented immediately as a daily percentage chart allocated between taxed and untaxed balances together with the overall Tax Exempt Percentage for the year. A sample is as follows:

New clients will be issued a special code to gain access to our investment portfolio.

More information can be found about us on BGL’s help page here.

We hope that you like our approach to providing timely and relevant actuarial certificates.

If you would like to take advantage of this service, please defer to BGL and their SimpleFund360 platform.

The latest Life Tables for 2020-22 have been released by the Australian Government Actuary at 13 December 2024. This updates the previous tables by 5 years (2015-17).

The average life expectancy has increased by 0.55 years to 85.3 for females and by 0.49 years to 81.3 for males (without further improvement).

Connectingthedots is pleased is offer a sample “Retirement Income Covenant” for use by SMSFs and superannuation trustees alike. We’re making setting retirement objectives seamless.